Building D2C Profitability with Cost Analytics | Cognitute

How Cost Analytics Helps D2C Brands Build Profitability Beyond Discounts

January 22, 2026

Digital Operations

How Cost Analytics Helps D2C Brands Build Profitability Beyond Discounts

Key Takeaways

- Sustainable growth depends on a clear understanding of unit economics and the ability to influence them through data.

- Cost analytics provides granular insight into CAC, contribution margin, fulfilment cost and return ratios, enabling leaders to make financially responsible decisions.

- Real brands across India and APAC have demonstrated that operational improvements driven by analytics can lift contribution margins by meaningful percentages.

- Scenario analysis strengthens decision-making by showing how product experience, fulfilment design and marketing discipline influence profitability.

- Organisations that embed cross-functional visibility and align incentives around contribution margin experience faster, healthier growth trajectories.

Growth in the D2C sector has accelerated across India and APAC. However, margins have come under consistent pressure due to rising acquisition costs, inefficient fulfilment, and high return ratios.

Cost analytics has emerged as a strategic foundation that allows brands to balance ambition with financial discipline. By unifying data across marketing, supply chain, product, and customer behaviour, leadership teams can control unit economics, predict profitability, and scale with confidence.

This article explains the strategic role of cost analytics, illustrates real outcomes using market-relevant data points, and includes two practical scenarios from well-known regional brands. It concludes with actionable recommendations and key takeaways for organisations that want to build high-growth, margin-positive D2C businesses.

Why Cost Analytics Is Central To Margin-Positive Growth

The D2C model promises closeness to the consumer and better control over product experience. However, many brands discover that direct access to consumers introduces new cost layers.

Acquisition costs have inflated significantly across Meta, Google, marketplaces, and influencer ecosystems. Logistics costs have risen with consumer expectations for faster delivery. Product returns remain a large operational drain in apparel, beauty, and lifestyle categories.

Industry analyses consistently indicate that brands that deploy granular analytics to guide marketing, supply chain and product decisions outperform their peers. Studies show that companies that use advanced personalisation see revenue uplift of approximately 5 to 15 percent and marketing efficiency improvements of 10 to 30 percent. These improvements directly impact contribution margin and unit profitability because they reduce reliance on high-cost acquisition and improve conversion of existing users.

In addition, fulfilment models that blend dark stores, pooled inventory, and batch delivery have shown meaningful cost reduction per order in Indian metros and GCC markets. Leaders that invest in demand forecasting and route optimisation reduce working capital, shrink wastage, and improve EBITDA margins.

Cost analytics is therefore not a measurement exercise. It is a strategic discipline that determines whether growth is sustainable or wasteful.

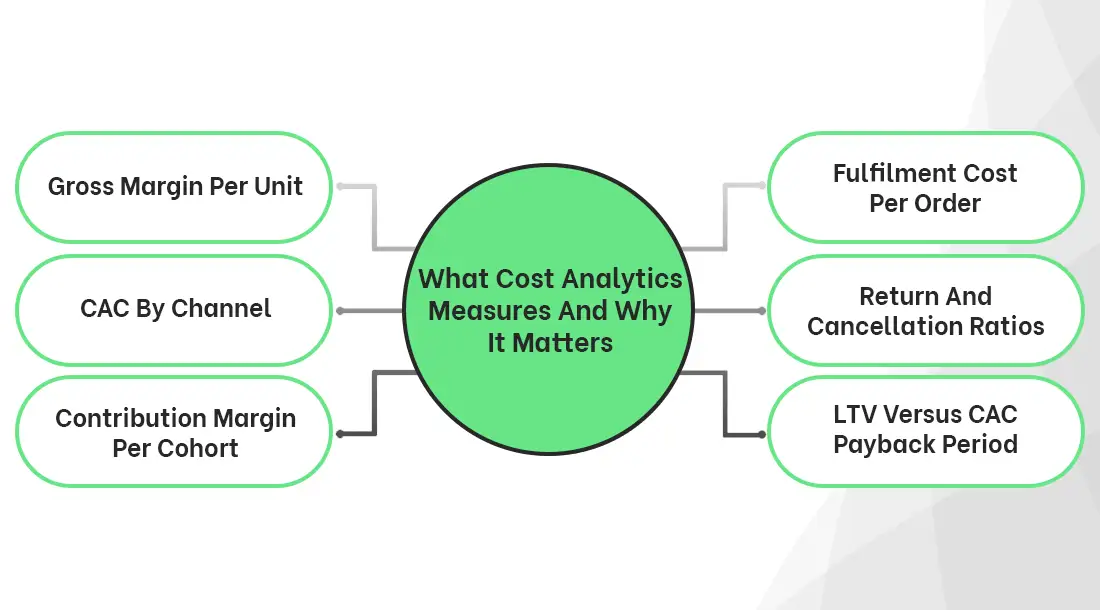

What Cost Analytics Measures And Why It Matters

A comprehensive cost analytics foundation includes a full-stack understanding of unit economics. Each metric plays a distinct role in protecting margin:

- Gross Margin Per Unit

Measures product-level profitability after accounting for COGS, packaging and any variable manufacturing costs. - CAC By Channel

Reveals the true cost of acquiring incremental paying customers. Granular CAC by audience segment, geography, and creative type is essential for budget optimisation. - Contribution Margin Per Cohort

Shows whether customers acquired in a particular period become profitable after factoring in returns, discount levels, logistic costs, and repeat behaviour. - Fulfilment Cost Per Order

Includes last-mile delivery, warehousing, picking, packing, and reverse logistics. Even small improvements compound over time. - Return And Cancellation Ratios

High return rates absorb operational bandwidth and logistic expenses. This metric uncovers product and experience issues that directly erode margins. - LTV Versus CAC Payback Period

A reliable payback model allows leadership teams to decide how much they can spend on growth without compromising long-term financial health.

When these metrics are analysed consistently and tied to decision-making rights, the organisation builds the capability to scale with discipline.

How Cost Analytics Transforms Outcomes

Consider the following scenario: A high-growth D2C fashion brand based in Mumbai was experiencing rapid top-line expansion but negative contribution margins due to return rates crossing 28 percent. The root causes included inconsistent sizing, poor product descriptions, and aggressive discount-led acquisition.

The organisation implemented SKU-level and cohort-level cost analytics. Return drivers were analysed at attribute level. Products with higher fabric stretch, unclear length details and inconsistent fit had disproportionate return ratios.

Actions taken included:

- Improving product detail pages with richer imagery and updated size guidance

- Suppressing discount-led campaigns for specific high-return SKUs

- Introducing predictive return scoring to manage inventory allocation

Within four months:

- Return ratios dropped from 28 percent to 18 percent

- Contribution margin improved by 9 percentage points

- CAC payback period reduced from 7 months to 4 months

This shift did not rely on top-line growth. It relied on cost analytics revealing operational inefficiencies that were hidden beneath a growing revenue number.

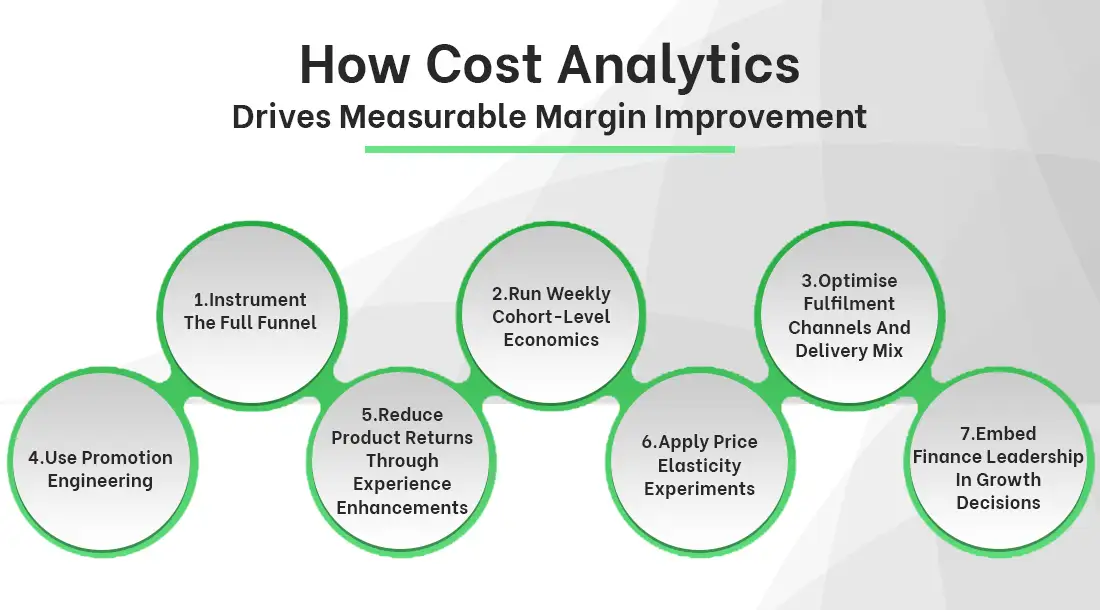

How Cost Analytics Drives Measurable Margin Improvement

Cost analytics becomes transformational when organisations operationalise insights across functions. The following steps help drive measurable improvement:

1. Instrument The Full Funnel

Connect marketing, product, CRM, fulfilment and finance into a single measurement environment. This enables full-funnel visibility from acquisition to repeat behaviour.

2. Run Weekly Cohort-Level Economics

Weekly reports reveal deteriorating cohorts early. When a specific channel produces low-quality customers with poor repeat intent, interventions become immediate.

3. Optimise Fulfilment Channels And Delivery Mix

Cost modeling helps identify where express delivery destroys margin and where pooled delivery can sustain profitability. Intelligent batching and route optimisation reduce per-order cost significantly.

4. Use Promotion Engineering

Rather than blanket discounts, target offers to customers most likely to convert with positive contribution margin. Predictive modelling helps identify users who have high full-price purchase propensity.

5. Reduce Product Returns Through Experience Enhancements

Better fit indicators, improved photos, detail-rich product descriptions and pre-purchase nudges help control return ratios and protect operational efficiency.

6. Apply Price Elasticity Experiments

Small price increases on high-volume SKUs can deliver significant improvement in gross margin without harming conversion.

7. Embed Finance Leadership In Growth Decisions

Every growth experiment should be supported by a clear contribution margin impact forecast and variance analysis during post-mortems.

Related Reads :

Driving Exponential Productivity Through Organizational Change

The Next Digital Transformation Wave in India

Organisational Foundations That Support Profitability

Analytics adoption succeeds only when organisational systems reinforce the discipline.

- Create A Shared Source Of Truth For Unit Economics

Common definitions of CAC, LTV and contribution margin eliminate debate and create decision clarity. - Establish Weekly Commercial Reviews

Consistent rhythm ensures that marketing, operations and finance review the same metrics and act promptly. - Reward Teams For Margin-Positive Growth

Incentives must favour contribution over superficial metrics such as impressions, clicks or raw revenue.

These cultural adjustments allow cost analytics to translate into sustained business outcomes.

Common Pitfalls That Reduce Margin

Many D2C businesses unintentionally undermine profitability. Frequent pitfalls include:

- Over-prioritising traffic over revenue quality

- Accelerating delivery speed without addressing underlying fulfilment cost structure

- Scaling campaigns without validating cohort quality

- Relying on blanket discounts that distort net revenue quality

- Ignoring product returns as a strategic lever

Avoiding these pitfalls requires integrating cost analytics directly into everyday decision-making

Final Thought

Margin-positive D2C growth is not achieved by limiting ambition. It is achieved by directing ambition with precision. Cost analytics allows business leaders to understand where value is created, where value leaks, and how each intervention affects long-term profitability. In a market where customer expectations continue to rise and acquisition costs remain volatile, the brands that win will be those that treat cost analytics as a strategic capability rather than an operational afterthought.

Read Our Other Insights : Agentic AI Revolutionizes Customer Support into Care

Authors

AVP, Digital Growth

.webp)

.webp)

.webp)

.webp)

.webp)

.jpg)

.jpg)

.webp)