Marico’s Digital Supply Chain Resilience | Case Study

Maricos Digital Supply Chain Resilience Compresses The Loop Between Demand Sensing and Execution

Key Takeaways

- Marico’s transformation is an operating model change that compresses the loop between demand sensing, planning, and execution.

- Advanced analytics and AI ML are positioned as supply chain accelerators, but only after master data, process discipline, and visibility are strengthened.

- Project SETU signals a strategic bet on improving GT execution through direct reach and higher quality distribution, not a retreat from traditional channels.

- D2C and digital first brands work best where AOV, repeat cycles, and differentiation can sustain CAC and fulfilment, as seen in the profitability trajectory of Marico’s digital first portfolio.

- For foods, Marico’s leadership is explicit that digital only economics are structurally difficult in India, which makes omnichannel scale essential.

- The end state is omnichannel clarity where GT, MT, marketplaces, and D2C have distinct roles in reach, profitability shape, and growth velocity.

For decades, FMCG leadership in India was built on one core capability scale. Win distribution, maintain availability, and run a supply chain that can feed millions of daily purchase decisions.

Post 2014, the market began to rewire. Demand started moving faster than planning cycles. Discovery moved to search and social. Marketplaces and quick commerce changed consumer expectations. And digital first brands proved that a product can go from niche to mainstream before legacy operating rhythms even notice.

Marico’s response is a useful blueprint for 2026 because it does not treat digital as a channel add-on. It treats digital as a redesign of how the enterprise senses demand, decides, and executes. Two moves sit at the center of the story.

- A digitised supply chain anchored in data and advanced analytics to improve forecasting and execution

- D2C and digital first brand acceleration, while keeping GT as the reach engine and improving GT quality through Project SETU

This case study breaks down what changed, why it works, where it does not, and what an operator should learn from it.

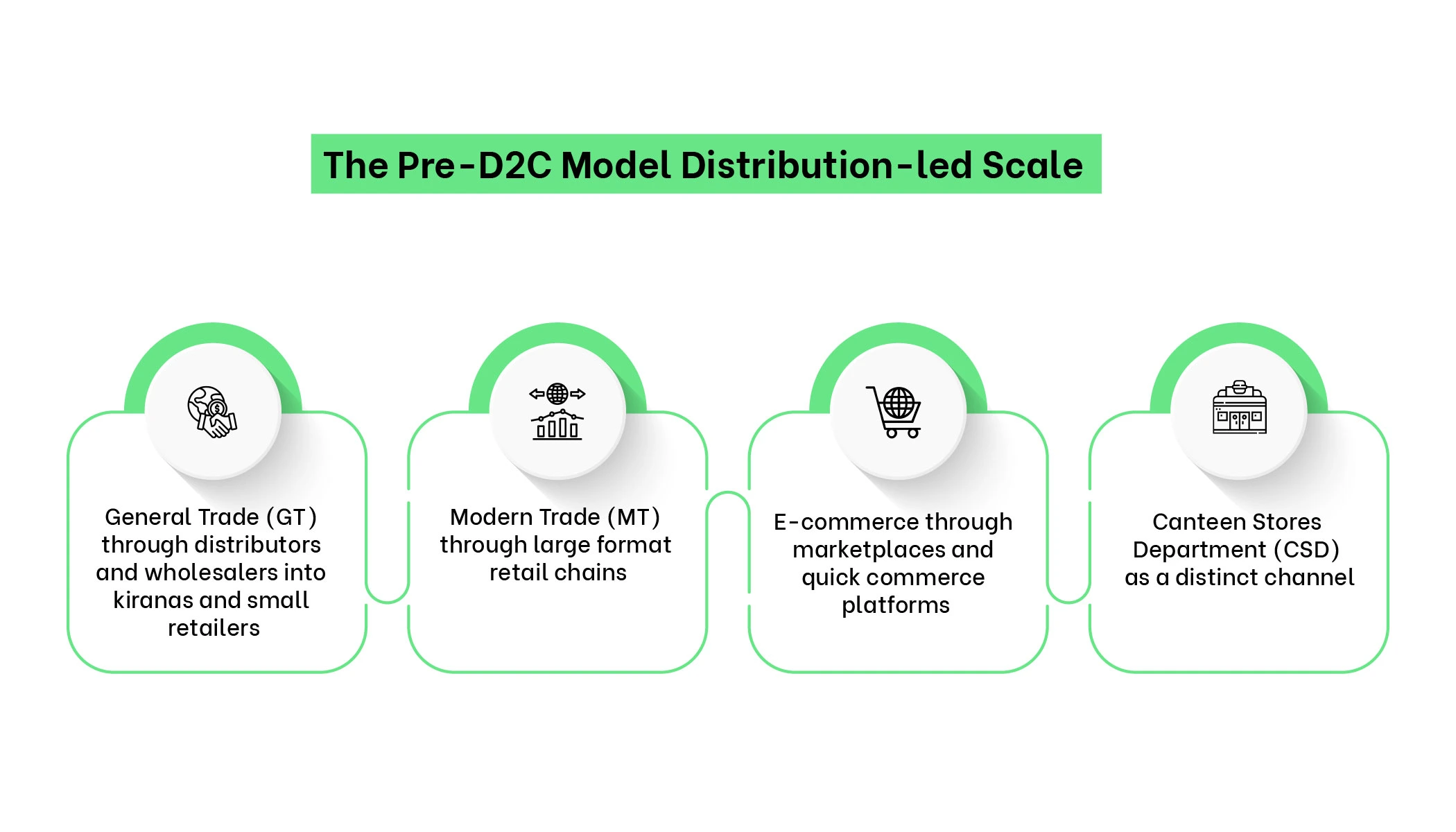

The Pre-D2C Model Distribution-led Scale

Before the D2C wave, Marico’s engine looked like a classic Indian FMCG route to market.

- General Trade (GT) through distributors and wholesalers into kiranas and small retailers

- Modern Trade (MT) through large format retail chains

- E-commerce through marketplaces and quick commerce platforms

- Canteen Stores Department (CSD) as a distinct channel

In FY14, GT represented roughly 81%, with MT plus e-commerce at about 11% and CSD at 8%. By FY24, GT was about 63%, MT plus e-commerce 30%, and CSD 7%. These numbers show that while GT still remains the largest engine of reach, MT and e-commerce are expanding faster and behave differently in demand patterns. Digital execution requires a faster planning and fulfilment cadence than the legacy system was built for.

The Supply Chain Shift From Forecasting To Decisioning

Marico has explicitly communicated its investment in advanced analytics and AI ML to streamline supply chain operations.

Modern supply chains do not win by producing a perfect forecast once a month. They win by building a system that updates assumptions continuously, detects exceptions early, and routes decisions quickly. This is the control tower idea in practice, a model widely discussed in high performing global supply chains.

Demand Signal Richness

Forecast accuracy improves when the signal improves. In FMCG, the most useful signals are rarely confined to historical shipments.

- Channel level velocity shifts that appear first in online and modern trade

- Campaign calendars and social spikes that produce short lived demand surges

- Stockout signals and lost sales proxies

- Ratings and reviews that hint at product issues and potential returns

Marico’s broader digital narrative highlights the value of real time signals and data driven decision making across the enterprise.

Inventory Health Not Inventory Level

Digitisation is also about inventory quality.

- Ageing stock by node and by SKU

- Service level and fill rate by channel

- Safety stock logic based on volatility and lead times

- Rebalancing triggers that move inventory before it becomes dead stock

This aligns with what advanced planning literature in CPG repeatedly emphasizes. The value comes from making planning more granular and responsive, not just more automated.

Exception Based Execution

In high scale FMCG operations, exceptions are guaranteed. The difference is whether they are handled late by firefighting or early by systems.

A mature digitised supply chain typically includes

- automated alerts when forecast error spikes

- early warnings on service level deterioration

- rapid decision routing across sales, supply, and logistics

This is the operating logic behind modern supply chain IT modernisation programs in global best practice playbooks.

ERP Modernisation Through Digital

Marico’s public transformation narrative includes an ERP modernisation and unification that typically enables

- one version of master data across SKUs, packs, and channels

- standardised transaction flows across procurement, manufacturing, and finance

- more reliable profitability views by SKU and channel

- faster close and tighter planning cycles because data reconciliation reduces

Without modernised data and systems, analytics cannot reliably convert into action.

Tech Enabled Distribution Project SETU And The GT Reinvention

The most underrated part of Marico’s story is that it did not treat digital as a replacement for GT. It treated digital as a force that requires GT to evolve.

Marico positions Project SETU as a multi year effort to expand direct reach and improve the quality of distribution through range selling and reduced dependence on wholesale behaviour that prioritises only fast movers.

In the same distribution narrative, Marico highlights IT and analytics enablement, including field and distribution tools and systems such as PDAs and named internal programs like ISRO and RETINA.

Operationally, this points to a clear intent

- improve outlet coverage and assortment execution

- increase visibility of secondary and tertiary movement

- strengthen frontline discipline so that analytics can be acted on consistently

This is how incumbents protect their biggest growth lever while becoming faster.

The D2C Acceleration Digital First As A Learning Engine

Marico’s investor materials label a digital first portfolio that includes Beardo, Just Herbs, Coco Soul, and Pure Sense.

Marico has also expanded through acquisitions and majority stakes, with Just Herbs being a notable example that moved from independent digital first brand to being part of Marico’s portfolio.

The strategic value of D2C for an incumbent is not only incremental revenue. It is learning velocity.

D2C creates a direct feedback loop across

- first party data on repeat behaviour and cohorts

- faster experimentation on bundles, messaging, and pricing

- clearer attribution between marketing actions and consumer response

- richer product feedback through reviews and post purchase behaviour

This is also where analytics led marketing becomes an operational advantage, not a reporting exercise.

.webp)

Categories Where D2C Worked Better

Marico’s earnings call commentary indicates improving profitability in the digital first portfolio, including Beardo reaching double digit operating margin and Plix delivering single digit EBITDA margin, with an aspiration for double digit EBITDA margins across the portfolio by FY27.

This points to the categories where D2C tends to work best.

- Higher gross margin headroom that can absorb CAC and fulfilment

- Repeat potential driven by routines and replenishment

- Differentiation that reduces pure price comparability

In practical terms, this is why grooming, beauty, and wellness often scale better through a D2C plus marketplaces entry and then graduate into wider distribution once product market fit is proven.

Where D2C As Digital Only Proved Insuffcient

Marico’s leadership has been explicit that a profitable digital only foods model is difficult in India and that foods need to get into GT for scale.

The economics behind this statement are structural.

- Lower AOV makes fulfilment a high percentage of the basket

- Returns, damage, and customer service add hidden cost

- Discounting pressure on platforms compresses contribution margin

- High frequency purchase shifts consumers to the most convenient channel, often offline or quick commerce

This is why the winning pattern in foods is usually omnichannel. D2C can still play a role in discovery, community, subscription, and premium cohorts, but GT and MT remain the scale engines.

Omnichannel Economics Roles, Ratios, And Tradeoffs

Marico’s channel mix illustrates why omnichannel clarity matters. GT remains the largest share while MT and e-commerce have grown meaningfully.

A useful operator lens is to treat each model as a different economic and execution machine.

General Trade GT

- Highest reach and deepest penetration

- Profitability often improves at scale, but requires trade investment and execution discipline

- Best suited for mass, high velocity SKUs and ubiquitous availability needs

Modern Trade And Marketplaces

- Faster discovery and urban scale

- Growth accelerates with platform visibility

- Margin pressure can increase through fees, discounting, and shared customer ownership

Direct To Consumer D2C

- Best for premiumisation, brand building, and first party learning

- Higher gross margin potential, but CAC and fulfilment can erode contribution margin

- Wins when retention and repeat behaviour are strong

CSD

- Steady institutional channel with stable demand patterns

The strategic maturity in Marico’s approach is that it is not choosing one channel ideology. It is building channel specific portfolios and execution systems that reduce conflict and protect unit economics.

The Tooling Layer Beyond One System

Large scale transformation rarely runs on a single platform. Public material points to an ERP backbone, IT enabled distribution, and unified social listening.

In a typical enterprise architecture that supports these outcomes, you would expect capability layers such as

- APS for demand and supply planning

- OMS for orchestrating orders across D2C, marketplaces, and MT

- WMS for warehouse accuracy and faster pick pack ship

- TMS for transport planning and freight visibility

- MDM for SKU, pack, and channel master data governance

- CDP and CRM for first party profile, segmentation, and lifecycle engagement

- Social listening and CXM platforms for real time voice of consumer and risk management, where Marico’s Sprinklr customer story is one example

The real differentiator is not the list of tools. It is integration, data discipline, and decision rights.

Closing Insight Speed Is Now A Supply Chain Feature

Marico’s story shows a clear 2026 truth for incumbents. Digital transformation is not a marketing initiative and not a software upgrade. It is an operating system redesign.

When demand shifts in days, the company that wins is the one that

- senses faster

- decides faster

- executes reliably across channels

In that world, speed is not a growth hack. Speed is a supply chain feature, a channel strategy, and a leadership discipline.

Read our Other Case Studies : Reliance Campa Cola Reshaping India’s Cola Market

.jpg)